For the love of money is a root of all kinds of evil – I Timothy 6: 9-10

Too many people spend money they haven’t earned, to buy things they don’t want, to impress people they don’t like – Will Smith

The above bible quotation is often misquoted as “money is the root of all evil”, but it is the love of money that is the problem. While happiness comes mostly from having good relationships with others and your emotional well-being, I think the chances of achieving these are greatly improved if you always ensure your outgoings are less than your income. That is, you are self supporting. By the time they reach middle age, most people would wish to have a comfortable life free of financial worry – in other words, having enough money set aside to cover any unexpected expense or loss of income now and in retirement.

Aging populations and falling birth rates, coupled with lower tax revenues and ballooning deficits as manufacturing and many service jobs move to Asia, have pretty much made the current social models of many countries unsustainable. Here in Ontario, half of tax revenues raised from all sources are spent on health care and, still, waiting lists for non-emergency MRI diagnostic scans are 2 to 6 months long. Since taxes in the province are already high, further increases would make us less competitive and lead to even higher unemployment and welfare costs. It seems that if we are looking to maintain our standard of living we will need to be prepared to pay an increasing share of healthcare and retirement expenses directly out of our own pockets.

With the exception of some mentally or physically incapacitated folk, no matter what their economic earning power, anyone can achieve financial security by working hard, living frugally, saving diligently, and investing wisely. My mother, father, and my grandparents all lived by this creed and, even though my dad suffered from diabetes, was legally blind and received a modest government disability benefit, our family was never in financial difficulties. My brother and I each had a set of clothes for working on our small farm, another for school, and one for Sunday school. These were replaced only when we wore them out or we grew out of them. Most of our food was home grown –vegetables, tomatoes, eggs and milk – meat, cheese and cereals were the main bought items. Entertainment was a weekly visit to the movies, and playing with my brother on the farm. The 1928 model A Ford car was only driven the two miles to town once a week to save on the cost of gasoline.

Not a penny was spent on alcohol, tobacco, or gambling which were considered a waste of money. Nothing was wasted and all expenditures were for necessaries and to improve the family house and farm buildings. The development of the small two-acre family farm absorbed most of my parents’ savings and represented their principal investment.

At a more general level, the wealth a person creates during their lifetime involves three basic ingredients:

Their ability to seek out and follow through on opportunities

Their willingness to take measured risks

Their ability to avoid unnecessary purchases, and to manage and invest cash flow

In this context I would like to give you my take on the four key activities I referred to above that will allow anyone to become financially self-sufficient.

WORK HARD

Always be looking to maximize the value of your labour and skills in the market place. And always undertake available education and work experience that will increase your value in the market place. This applies equally whether you work in agriculture, the service industry, the trades, small business, a large company, or the professions. Don’t be afraid to relocate to a different employer, town, or country to maximize the value of your education and work experience. As one observer noted after a recent business downturn, loyalty is a one-way street when costs have to be cut. So, while loyalty is a desirable attribute, it should not override your duty to look after your own long-term interests. My own work/study experience is an example of sorts:

My formal work life started when I was eleven years old and worked weekends for Reg Joe in his market garden at Alma outside Oamaru for one pound five shillings ($2.50) a day. The work was hard but my brother and I were “as pleased as Punch” when we collected five pounds between us from Reg each Sunday night.

Reg was one of the hardest workers and the most frugal person I ever did meet. You can read about his story in an Otago Daily Times’ article .

Weekdays, I studied accounting, English, math, and other subjects at Waitaki Boys’ High School. At seventeen I relocated to Dunedin after graduating from high school to work for the public accounting firm Barr, Burgess & Stewart and studied part time for a bachelor’s degree in commerce at the University of Otago. At twenty years I spent twenty four months studying full-time at Otago to complete the BCom degree in accounting, a BA degree in economics, and my professional accounting designation. The New Zealand government covered most of the costs of my undergraduate education but I paid for my living costs during my period of full-time study by working vacations at the Waitaki Farmers’ Freezing Company’s Pukeuri meat packing works. The work in the gut house was extremely dirty and mind numbingly tedious, but the unionized pay was very good.

At twenty two I moved to Australia and worked at the Melbourne office of Arthur Andersen & Co., the world-wide Public Accounting firm, and transferred to its Vancouver, Canada office two years later. I left AA&Co at twenty five to study for a two-year MBA degree at the University of Western Ontario’s graduate school of business in London, Ontario. The Bank of Nova Scotia’s head office hired me in Toronto in 1975, and I retired from BNS, one of Canada’s largest financial institutions in 2005 as a Vice-President after working in four different divisions.

LIVE FRUGALLY

Live a healthy lifestyle but don’t buy things you don’t need. Wanting something is not the same as needing it – don’t waste money on unnecessary things. Personal finance author Lesley Scorgie offers the following top ten spending tips in her book Rich by Forty:

1 Get ruthless. Set your priorities straight and be ruthless about sticking to them. When retirement savings are more important than going to the movies, plow that money into your retirement savings plan.

2 Get active. If you’re used to driving, try taking public transit, carpool, walk, run, bike, or inline skate instead. Entertain yourself by getting active.

3 Get healthy about your food habits. If you smoke or drink, stop. Cook at home rather than eating at restaurants to avoid the fat salt and sugar they add to their food, and buy food in bulk.

4 Get cheap entertainment. Borrow books, CDs, magazines and DVDs from your local public library. Sign your kids up for free programmes. Rather than going out for expensive evenings with friends, go for a walk or play board games. If you like to travel, stay closer to home. Drive to a destination rather than flying. Look for travel specials.

5 Get negotiating. Always ask for a discount especially if you are paying with cash and buy the things you need on sale. But remember, if you don’t need it don’t buy it no matter how good the sale is – a good deal you can’t afford is never a good deal.

6 Get a bargain. Buy used through local websites, eBay, Craigslist, TradeMe, garage sales, estate sales, and auctions.

7 Get the minimum. Pare down your purchases. Closely check all your expenses and make sure you are not purchasing any unnecessary bells and whistles.

8 Get environmentally friendly. Save on utility bills by washing laundry in cold water, turn the temperature down a few degrees in your house, turn the lights out, unplug electronic equipment when you are not using it, and properly seal your doors and windows. Reuse and recycle.

9 Get smart about maintenance. Do your own. Many people pay others to do things they could do themselves.

10 Get rid of excess credit. Cut up all but 1 or 2 credit cards. Keep the one with the longest history and the lowest annual fee and interest rate. If you struggle with credit card temptation, get the cards out of your sight. Certainly do this if you do not consistently pay off the balance of every card each month.

My early years working in Dunedin at the accounting firm of Barr, Burgess & Stewart were marked by quite a high level of frugality. Out of my $15 weekly salary, I paid half in room and board, half of what was left on university and living expenses, and saved the rest. My landlady, Mrs. Tubb, used to make me a cut sandwich lunch each day and provided me with breakfast and dinner as well – all included in my boarding fee. Local transportation used to cost me nothing since I used to ride the bicycle I got when I was ten years old to the office and to the university for morning and evening lectures – although it did cost me a new pair of good trousers when my bike skidded on the pavement and I fell off one frosty morning on the way to work!

For those folk who have a really hard time controlling and keeping track of their spending, I think the arrangement used by Mrs. Tubb to control her household expenses could be very helpful. She dealt entirely in cash to avoid bank fees and to give herself budgeting simplicity. Every two weeks when she received Mr. Tubb’s wage envelope and our boarding money she would allocate all the cash into a dozen or so screw-top bottles – one for savings, one for vacations, one each for his and her allowances, one for an emergency fund to cover house repairs, etc., one for food, one for property rates and taxes, one for power, one for gas, one for car expenses, and so on until all the household expenses had been covered. As each expense was actually paid, she took cash from the appropriate bottle and replaced it with a receipt or a note listing the expense. She controlled her cash flow on an on-going basis, and also easily made quick income and expense listings at the end of each year and during the year. She deposited her savings, vacation, and emergency fund allocations to special purpose savings accounts to earn interest until the funds were needed.

In the six years I spent with Mr. and Mrs. Tubb, the ‘bottle budgeting system’ seemed to work very well with a minimum of effort and never once did I notice any situations that indicated a shortage of cash or financial problems.

SAVE DILIGENTLY

Always ‘pay yourself first’. Put at least the first ten cents of every dollar you earn into an on-line no-fee savings account to be invested in assets to secure your long-term financial future. This will be your Investment Savings Account. Have your bank set up an automatic transfer from your Chequing Account to your on-line Investment Savings Account each pay day.

Budget carefully to live on the remaining 90% of your income and transfer anything you have left over at the end of each month into an on-line no-fee savings account to keep you afloat in the event you lose your job, or some other financial emergency comes up. This will be your Emergency Savings Account. When the balance of this account is enough to cover your on-going expenses for six months, put the money you have leftover each month into your Investment Savings Account to further boost your savings for investment purposes.

Margaret Atwood, a Canadian author just a little older than I am, penned her best-selling book Payback: Debt and the Shadow Side of Wealth during the 2008 world-wide financial meltdown. In an interview she offered some comments on saving and debt that largely mirror my experience and thoughts on the subject:

Saving and debt have interested me for some time – what with my little red bank book when I was 8 and the fact that, growing up, my generation had quite a different attitude to going into debt. Everything changed in the ‘70s when credit cards were deployed. They made you feel richer than you were, so people went out and spent money, and then realized it was a loan. Credit cards changed a whole generation who now aren’t used to not having things. The concept of saving up and getting it when you can afford it, that’s not how they think. Now they think, I’m worth it, I owe it to myself therefore I’m going to have it now. We’ll worry about later, later.

Learning to save is a bit like learning a foreign language – the sooner you start the easier it is. It really is important for children to experience the saving habit very early in life. Atwood’s memory of her little red bank book resonates well with me in that my mother opened a Post Office Savings Account for me when I was two years old. My earliest “financial” memories are of putting the small sums of money I received from my grandparents on my birthday and at Christmas through the small hole in the little red metal box that came with the account. Any other money I received from cashing in the deposits on beer bottles I picked up in the long grass by the main highway also went into the metal box, and once a year or so mum would take my brother and me to the Savings Bank to make deposits into our accounts. In the early years she would lift us up onto the counter so we could watch as the teller opened the tin boxes with a special key, counted the cash, and made the deposit into our savings passbooks – unlike Atwood’s, ours had a picture of a wise squirrel saving nuts for the winter on the front. Saving for us was a very serious business indeed and since it was practised from an early age it became the default action whenever we received money.

Successful saving is really about impulse management. The answer to increasing our personal savings rate is not just about giving people more knowledge –they are not idiots and know for instance that eating right, exercising regularly, and saving are obviously in their own best interests. In addition to educating people about calorie counts and the true cost of retirement, it would be very helpful to find ways to boost impulse management and the capacity for self control which are key traits to much success in life. The famous 1970s marshmallow experiment introduced four-year-olds to a man who had some marshmallows. He showed them a plate with one marshmallow and a plate with two marshmallows, and asked them which one they would rather have – the one with two marshmallows of course! He said he had to leave the room for five minutes and would take the plate with two marshmallows with him. If they didn’t eat the one marshmallow while he was away he would give them the two marshmallows when he returned. The experiment had extraordinary predictive powers. The children who were able to resist the temptation for instant gratification studied the hardest and wound up in the best universities. Even at such a young age they understood the benefits of deferred gratification.

INVEST WISELY

The first principle of investing, as the ‘old school’ Rothschild bankers used to insist, is to preserve your capital. The second is to diversify your assets into safe investments to provide a balance between current income, long-term capital gains, and liquid cash balances. My long-term financial goal is to diversify my risk by having a third of my assets in company shares, a third in property, and a third in high quality bank deposits.

Your first investment assets will likely be savings account deposits, term bank deposits, and company shares, with your property assets coming later when you buy your first home.

SHARES– There are many schemes offered by the financial community to allow people to invest in shares, but most are set up to line the pockets of their sponsors, arrangers, managers, brokers, salesmen, advisors, lawyers, and various other financial parasites – not to mention the straight out crooks and incompetents in the business. I have found the following arrangement best for developing a good share portfolio to provide a balance of capital gains and dividend income:

I deal only with large, reputable financial institutions, or their wholly-owned subsidiaries. Never pay your investment funds to an agent or other middle man. There have been too many instances of these funds being misappropriated. Bernie Madoff scammed hundreds of wealthy clients out of billions of dollars in the US when he spent their investment funds. He employed an elaborate accounting system to provide his clients with fake statements of their investments. He died in prison while serving a 150 year sentence

If you are a resident of New Zealand, you might well deal with ANZ Bank, a wholly-owned subsidiary of the Australian ANZ Banking Group, and New Zealand’s largest bank. ANZ has entered into a service arrangement with Jarden Direct who offers a Share and Bond Trading Account for New Zealand residents and you can open one of these via their website at https://onlinestore.anz.co.nz/get/securities . NOTE: You should check that ANZ formally stands behind Jarden’s service.

I think a sensible strategy would be to every two or three months or sooner when you have a thousand to fifteen hundred dollars in your Investment Savings Account to buy a minimum block of twenty five shares in one of the hundred largest corporations listed on the Australian Stock Exchange (the ASX100). From this group I would pick three of the major Australian banks – ANZ Banking Group (ANZ), Commercial bank of Australia (CBA), and Westpac Banking Corp (WBC) – to buy shares in. At the time I write this these banks are well managed, capitalized, and regulated, and are representative of the strong Australian economy and currency. Although they are exposed to major downturns in the resource sector, over time, they are expected to continue producing increasing revenues, profits and well-covered dividends. These are often referred to as ‘great stocks’. The stock prices of companies without these attributes often fluctuate wildly or stagnate for long periods of time and are referred to as ‘grief stocks’!

The dividends the banks pay usually give a return of about 6% p.a. on the current cost of their shares. I would purchase shares of these three companies in turn – first ANZ, then after my Investment Savings Account balance had built up again CBA, and when it builds up again WBC, then ANZ again, and so on. The cost of each purchase and the brokerage commission would be taken from your Investment Savings Account and the shares you purchase would be held in your Share and Bond Trading Account.

With this continuous purchasing of shares every two or three months, the cost of your share portfolio averages out over high-priced and low-priced market periods and you don’t have to worry about trying to buy at the ‘right’ time. You would receive a stream of dividends every six months and this would increase steadily as the number of shares in your account increases and as each company increases its dividend. These dividends would be paid into your Investment Savings Account and as they accumulate along with the transfers from your Chequing Account, they are used to buy more shares. This is called ‘compounding returns’ since as time passes you will earn dividends on the dividends that you have reinvested in more shares. In the mean time the market value of the shares in your Share and Bond Trading Account will themselves fluctuate, but will most likely increase over the long term as each company grows its business, profits and dividend per share. Some experts would argue this kind of portfolio is not diversified enough to avoid a major crises in the Australian banking industry. But you would be spreading your risk over the three industry leaders whose customers are in many different businesses and each bank’s risks are closely monitored by the Australian banking regulators. Many of their customers are located around the world which spreads their risks further.

In Canada, as a Canadian citizen, resident, and taxpayer, I deal with Scotiabank’s wholly-owned subsidiary Scotia iTRADE, a discount broker. I have Scotiabank transfer money automatically each two weeks from my Chequing Account to my Cash Share Account, and when the balance builds up I go on-line and buy, in turn, shares in the top three Canadian banks – Royal Bank of Canada, Toronto Dominion Bank, and Scotiabank.

As the cash from my Chequing Account and the dividends from the shares I purchase accumulate in my Scotia iTRADE Cash Share Account and are used to buy more shares, my returns compound. These three Canadian banks currently pay dividends each quarter equal to around 3.5% p.a. of their current valuations. At the time I write this, these banks are well managed, capitalized, and regulated, and are representative of the strong Canadian economy and currency. Their business lines and assets are diversified, with growing assets and profits. Their dividends increase over time, and are well protected with dividend payouts typically just less than half their profits. If you are a Canadian resident you can open a Scotia iTrade Cash Share Account at http://www.scotiabank.com/itrade/en/0,,3766,00.html.

By holding shares in a relatively small number of high profile companies in one industry I can keep up-to-date on their financial soundness and profitability by following their coverage in the financial press and reviewing their interim and annual published financial reports. I intend to hold these three Canadian stocks through good and poor economic cycles and the related share price fluctuations as long as they remain financially strong with increasing revenues, profits, and dividends – the hallmark of “great stocks”. Recent developments in the financial technology (“Fintech”) sector will, though, need to be closely watched.

The financial technology industry represents a rapidly growing group of internet start-up companies which is threatening to disrupt the banking industry model and cut deeply into the banks’ business and profits. They have developed alternative payment systems such as “Apple pay”, algorithms to provide small business loans, “Robo advisors” to provide personal financial advice, and the like. The banks’ responses have been encouraging.

Scotiabank for instance has acquired Ing Bank’s low-cost on-line deposit gathering subsidiary. They have also agreed to provide their customers with Apple Pay as a payment option and small business loans through Kabbage the on-line start-up business loan provider. (Perhaps following Machaivelli’s advice to, “Keep your friends close and your enemies closer!”) Scotiabank is also trimming its branch and head office payroll and is redeploying the savings into a 500-person “Tech Factory” headed by a recently appointed Silicon Valley executive.

PROPERTY – I have found residential property is the best place to invest rather than commercial property which tends to fluctuate much more in step with changes kin the economy. My wife and I own our family home in Toronto, a low maintenance two-storied three-bedroom brick residence built in 1948. My brother and I originally bought the house in 1976 when we were twenty eight years old. It is located in a small mid-town neighbourhood.

The purchase was a big stretch for us financially. Actually, we borrowed 100% of the purchase price with a 75% first mortgage from our employer Scotiabank, a 15% second mortgage from the vendor, and a 10% staff loan, with the closing expenses going on our credit cards. I would not recommend this level of debt financing for a house purchase unless the owner(s) have a very stable and adequate source of cash flow – my brother and I both had stable jobs in Toronto with Scotiabank, a financially strong employer. Since we were still single, we devoted most of our after-tax earnings to paying off the high interest credit cards first, and then the second mortgage. And, since the staff loan was costing us just 3% interest, we then applied any other cash we had to prepaying the 13% first mortgage.

As an aside, inflation was very high in the late 1970’s and after we had purchased the house interest rates were hiked up to 20% to choke off consumer demand and bring prices down. So, while it was tough paying the 13% mortgage to start with, we were getting 18% pay increases and after a year or two the monthly fixed mortgage payments became a much smaller portion of our take home pay and much easier to handle. This supports the old saying that inflation is a borrower’s friend and a lender’s enemy.

It is very important to protect your real estate investment in the early stages by taking out mortgage insurance that will pay the balance of the mortgage off in the event one of the owners dies or goes on long-term disability. The insurance is fairly expensive especially at a time when your cash flow is tight but I believe it is well worth while. You might cancel the mortgage insurance when the salary, cash flow or cash assets of either partner can take care of the mortgage if anything untoward happens to the other owner. And make sure your property is always insured against loss by fire, flood, earthquakes and other hazards.

When you enter the residential property market I think it is wise to buy the best house you can afford in a desirable neighbourhood, and which allows good scope for upgrades, extensions and improvements. Location is very important. As well as providing desirable, family-orientated neighbourhoods Toronto’s house values are underpinned by net immigration of about 100,000 people a year. Many of these folk are fleeing violent, corrupt, or economically depressed homelands. Many are also financially well off and purchase homes on arrival. Others begin renting, trade up to lower priced condominiums and then suburban homes as their equity and cash flow permits.

After five years my brother located to Scotiabank’s New York office and my wife and I bought out his share of the increased equity in the house and renewed the mortgage in our names which we eventually paid off six years sooner than the sixteen years that remained on the amortization. We were able to do this by applying each annual salary bonus we received from Scotiabank as a prepayment against the mortgage– but only after we had enough money set aside in our savings account to take care of any financial emergencies.

I believe a mortgage-free home should be one of the cornerstones of a financially secure retirement. Our Toronto house was purchased in 1976 and has greatly appreciated in value to the present time. We have made additions and improvements over time to meet our family’s needs rather than moving and incurring real estate fees.

Shortly before our retirement in 2005 I purchased our stucco-over-brick New Zealand vacation cottage. Again, the value of the cottage is underpinned by its location. The cottage fronts onto the picturesque Otago Harbour with a spectacular view of the city across the water. It’s on a good city bus route and it is a fifty minute walk to the town centre.

While Dunedin is a university town with very little population growth, the location and physical attributes of the property have caused it to increase in value but, unfortunately, the New Zealand dollar has depreciated against the Canadian dollar by about the same amount.

A closing word on real estate investment: It is always difficult to save the necessary 20-30% down payment on a residential property to either live in or rent out, but you can do this much earlier if you collaborate with a like-minded person or small group. A family grouping such as my brother and I used can work well or a tight group of three or four compatible investors with a written agreement covering all aspects of the undertaking can also work. An ideal arrangement would be for three or four young trades-people to enter into a formal partnership to acquire a poorly maintained property in a good residential neighbourhood and renovate it to rent out. This would work particularly well if the members of the group were qualified in, say, the carpentry, electrical, and plumbing trades. To strengthen the arrangement, mortgage financing could be avoided by having other family members or professional people with spare funds provide the balance of the purchase price as additional equity funding. The partnership agreement should be drawn up by a qualified and competent lawyer and should cover the partnership objectives, and important issues such as the share each partner is to receive for their cash or labour contribution, how the completed property is to be valued, and the circumstances that will allow or require a partner to exit the partnership or for the partnership to be wound up. It is really important in this kind of arrangement to have good legal and accounting support or the thing is likely to fall apart at the first sign of disagreement between the partners. It is especially important for the partnership objectives to be set down in some detail and that each partner formally acknowledges and agrees to them before coming on board. Ideally, the partners would repeat the purchase – renovate – rent process with successive properties and equity investors and build a portfolio of rental properties with increasing values and rental revenues.

Whether your investment is in one house or in a portfolio of properties, it is extremely important to protect it by ensuring minor property repairs are attended to as they become necessary and to maintain a fully funded maintenance fund to take care of major long term repairs to roofs, heating plants, hot water systems and the like. Sufficient funds – possibly ten to fifteen percent of rentals – should be set aside and be invested in term bank deposits to meet upcoming repairs specifically identified by annual property reviews. A hot water heater may likely need replacing every twenty years and a roof may need resurfacing every fifteen years. And don’t underestimate the absolute importance of thoroughly vetting the financial and personal references of rental applicants. Get a credit bureau report and check the length of employment with the applicant’s present employer. Check with the applicant’s prior landlords to see if there were any tenant issues. Don’t rent to anyone who has financial problems or has a history of not honouring their tenant obligations. Taking on unsatisfactory tenants can cost you a great deal of money in unpaid rentals, legal fees to evict them, and repairs to damaged property.

If you find individual property investing is too time consuming or beyond your level of competence, consider a real estate investment trust – REIT – or other sizeable and professionally managed real estate investment vehicle. But do your homework before investing. Make sure the REIT or company is investing only in completed, well tenanted, quality office buildings in major cities. Check that the overall tenancy book has tenancy renewals spaced out over the next ten years to allow for a steady increase in rental revenues. Confirm there is professional management in place, that administration expenses are reasonable, and avoid investment arrangements involving conflicted management or shareholders. There should be no middlemen to bleed the entity by way of fees, commissions, profit sharing, and other self serving arrangements. Review the audited financial statements and annual reports to see if the return on your investment will be sufficient, > 5% cash flow return plus capital gains. Your prospective investment vehicle should not carry too much debt, <25% of the property values, any it does carry will mature evenly over, say, the next ten years. There should be a sinking fund based on regular engineering reports which detail major repair bills expected over the next twenty years, all backed by suitable cash reserves.

CASH – In order to ride out economic downturns and to sleep well at night, it’s important to keep good cash balances. Roughly a third of your net assets should be maintained in term interest-bearing certificates of deposit issued by the major Canadian banks, all covered by the Canadian government deposit insurance scheme.

.

.

The deposits are ‘laddered’. In other words in order to receive the best rate, the term of each deposit is for a period of five years, but one fifth of the total deposits mature each year to be reinvested at the then current rate for five years. In order to get to this situation, at the very beginning you would invest one fifth of your total deposits for one year, one fifth for two years, and so on up to five years. As each of these deposits matures then reinvest it for five years.

KEEPING SCORE

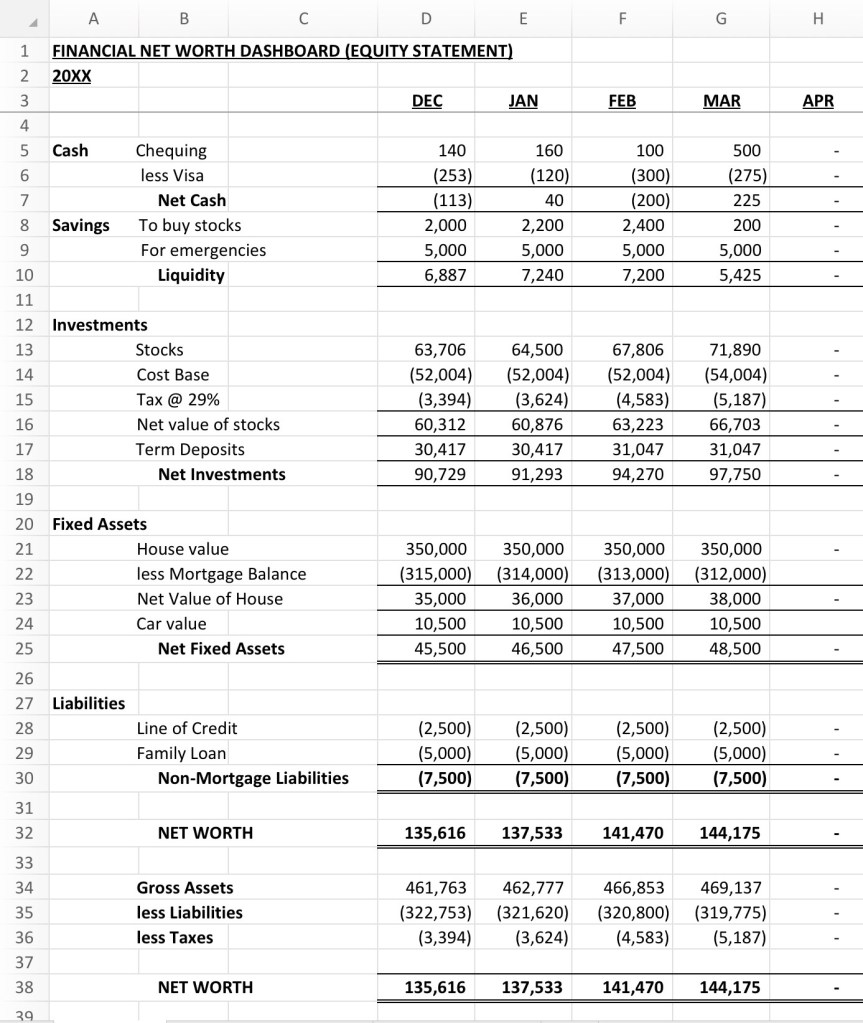

As with most things worth doing, people are motivated by tracking their progress over time and this also applies to building financial independence – giving support to the old saying that to effectively manage anything you need to measure it. I have found the best way to do this is to compute your Liquidity and Net Worth at the end of each month. Your Liquidity is your cash and savings account balances that are immediately available to you, and your Net Worth is arrived at by subtracting what you owe from the value of what you own.

To compute these items you will need to prepare a spread sheet with your assets and liabilities listed down the left hand side and headings for thirteen columns across the top – the closing balances of the prior year, and one for each month of the current year. You can set this up in a columnar exercise book or on an Excel electronic spread sheet on your computer. The electronic spreadsheet takes a little time to set up but will save you a great deal of time by automatically computing totals and sub totals. Once set up the monthly computing of your Net Worth should only take an hour or so.

To set up your spread sheet, first list your Liquidity (cash and savings accounts less credit card debt) starting at the top of the left hand side of your sheet and then sub total these for each column across the page. Next, list and total your Share (Stock) Accounts and Term Deposits. For “tax-paid” Share accounts be sure to deduct an allowance for taxes on the surplus of the current value of your shares over their purchase price. And then list and provide a total of the current valuations of your Real Estate properties net of mortgage debt. Finish this part of the spreadsheet by listing and totaling any other significant Sundry Assets you own such as automobiles etc. Finally list and total your Loan Accounts to arrive at your total Non-Mortgage Liabilities, and subtract this total from your Asset balances to show your Net Worth.

The aim is to increase your Net Worth each month, with the emphasis being on savings, the increase in the value of your investments, and the reduction of your debt, rather than on your monthly salary or wages. In other words, it is better to earn $1,000 a month and save $150 than to earn $10,000 a month and spend $11,000! That is, increasing Liquidity, Investments, and Net Worth are better indicators of your future financial prosperity than your salary alone.

I’ve read that money problems are the biggest cause of family disagreements and I have seen this many times for myself over the years. So while money in no way defines a successful life I do believe a sound financial footing is the underpinning of a happy and contented life. I’ll leave the final word on personal finance to a young acquaintance of mine who lives with his parents and saves a quarter to half of his take home pay. He remarked “I’ve seen just about everyone of my friends struggle financially. They’re killing themselves and I’m thinking to myself that I’m not going to live like that”.

On a wider front, becoming financially self-sufficient is much more urgent now than it used to be given the nature of our politics and demographics across the western world. With very few exceptions, politicians bent on hanging on to their elected positions continue to promise government services and benefits our countries cannot afford. Since the very same politicians don’t want to irritate the voters with tax increases, the shortfall is covered by domestic government bonds and foreign debt – all with a sadly predictable result.

New Zealand’s near financial meltdown in the early 1980’s is a good example of how these things usually unfold. Until then the government was all things to all people – free healthcare, average-wage welfare, farm and food subsidies, high minimum wages, union rights, import controls, free education to university level, and large government-financed infrastructure projects, etc., etc. Marginal tax rates were raised to 67 cents in the dollar and in addition to choking off productivity – most people preferred to ‘go fishing’ rather than give the government two thirds of their overtime money – it simply wasn’t enough to bridge the spending gap. The gravy train ended in the early ’80s when the Minister of Finance advised the Prime Minister and Cabinet in emergency meeting the international bond traders were unable to roll New Zealand’s outstanding bonds – never mind granting the country additional credit. The crisis was not wasted and the government of the day responded in the only way it could – import restrictions lifted, restrictive labour laws loosened, practically all subsidies withdrawn, substantial university fees introduced, the exchange rate floated, and so on. As a result New Zealand has gone from being one of the most restrictive countries in which to do business, to one of the most open.

I was in Canada when New Zealand’s spendthrift ways came to a screeching halt and recall watching an episode of the Canadian Broadcasting Corporation’s television investigative programme The Fifth Estate which took a look at the financial crisis and the resulting fallout. It started with three examples that vividly demonstrated the country’s greatly reduced financial circumstances – A hippopotamus had just given birth at the Auckland zoo, but the joyous and rare event was immediately overshadowed by the fact there were no funds available to expand the hippo enclosure and buy additional feed for the new arrival. So they shot him. The next segment showed a graphic shot of a badly corroded Auckland city sewage outlet leaking raw sewage into the picturesque Waitamata harbour. There were no funds to replace it so the council simply posted “No Swimming” signs and carried on. A small community on the South Island wanted a local police presence so an officer was transferred from the city after the community collected funds locally and built a small police station. The local Ford dealership sponsored a police car which was adorned with the dealership logo.

Twenty five years on, the rest of the world is at various stages in coming to grips with their own version of New Zealand’s unsustainable spending/debt problem. Former “middle class” folk are living in tent cities in Sacramento, the Californian state capital, as a result of unsustainable state spending and reckless bank mortgage lending.

Public sector unions are rioting in the streets of Athens as the Greek government puts an end to public sector worker and social entitlements – restrictive work rules, six weeks vacation, retirement at fifty seven and generous indexed pensions. Greece, like New Zealand, could not roll its bonds and after a tense few weeks received a bailout loan from Germany its biggest trading partner in the Euro zone.

Canada is not immune to these problems either. As the baby boomers age, the cost of “free” healthcare in Ontario absorbs fifty cents of every tax dollar the provincial government raises. And with the oldest at just sixty four, we boomers are only getting started on breaking the latest social safety net we’ve encountered! It’s the fall of 2010 and the local Toronto council elections are underway. I encountered a young candidate at my door who proclaimed he needed my vote to fight to ensure the provincial government paid a bigger share of Toronto’s (bloated) spending and reduce the city’s deficit. He seemed genuinely nonplussed when I pointed out to him both the provincial and the federal governments were running huge deficits following the recession and his voters were on the hook for those as well. He reluctantly agreed it was pointless shifting deficits around and each level of government needed to make its own spending cuts. This idea seems also to be lost on the provincial premier who has just introduced “free” full-day kindergarten for all the province’s four year olds – a multi-billion dollar annual programme to be laid on the back of an existing twenty billion dollar annual provincial deficit. As laudable as such a programme is, these things need to be paid for and more government borrowing only defers the cost to future generations and squeezes future government budgets with increased borrowing costs.

If government budgets and spending are not brought under control, bond interest costs will be driven up and the borrowing spree will end. As New Zealand learned, it’s much less painful to take care of these things earlier rather than later. And Thomas Jefferson’s remark, “A government that is big enough to give you everything you want is also big enough to take away everything you have,” resonates in these debt-laden times.

The takeaway from all of this is Government entitlement programmes such as education, healthcare and pensions will almost certainly be severely curtailed in the future. And I think young people in particular would be very wise to make sure they are prepared to pay for an increasing share of these services out of their own pockets.